The Gas Turbine Industry is Gaining Altitude

The Gas Turbine Industry is Gaining Altitude

The industry has hit some bumps in recent years, but the long view provides plenty of reasons for optimism.

The view from 30,000 feet is the common business idiom, meaning taking a step back and surveying the entirety of a situation. That distance, around 5.5 miles, isn’t random. Instead, it is the rounded down cruising altitude of modern jetliner like a Boeing 737 or an Airbus A320. The view from 30,000 feet, then, is what one sees when looking out the window in the middle of a long flight.

From the 30,000-foot perspective, the broad gas turbine industry falls into relatively few categories. The largest by far is commercial aviation, the jet engines that support the view from that altitude. Two others of smaller magnitude, military jet engines and gas turbines for electric generation, account for most of the rest of the industry.

Sometimes, however, even small markets can play an important role. Take, for example, mechanical drive gas turbines, the production of which accounted for $2 billion in 2021. That’s nothing to sneeze at, but from the perspective of the value of production for the entire gas turbine industry, which according to Forecast International (FI), a market research firm in Newtown, Conn., totaled $61.6 billion in 2021, it might be easy to overlook.

Three streams of airflow pass through and around the hot section of GE Aviation’s XA100 jet engine. The third stream (in blue) can be diverted to either add thrust or cool the engine so it can run hotter.

Image: GE Aviation

Mechanical drive gas turbines have a variety of applications, but a major use is powering natural gas pipeline compressors, using natural gas as fuel. The compression stations are typically spaced 100 kilometers apart to maintain pipeline flow and pressure, which can reach 1,000 psi, and are usually obscure support nodes in the national energy infrastructure.

Three streams of airflow pass through and around the hot section of GE Aviation’s XA100 jet engine. The third stream (in blue) can be diverted to either add thrust or cool the engine so it can run hotter.

Image: GE Aviation

Mechanical drive gas turbines have a variety of applications, but a major use is powering natural gas pipeline compressors, using natural gas as fuel. The compression stations are typically spaced 100 kilometers apart to maintain pipeline flow and pressure, which can reach 1,000 psi, and are usually obscure support nodes in the national energy infrastructure.

The importance of this gas turbine use was dramatically illustrated during the power crisis following the severe winter storm in Texas in February 2021. The large-scale, days-long blackout had multiple causes, but one major contributor was the failure to winterize pipeline facilities such as the compression stations. Compression station control systems malfunctioned along with other effects caused by the short-sighted economies of non-winterization, halting their function and resulting in natural gas power plants going offline for want of pipeline gas. This led to the worst energy infrastructure failure in Texas history, leading to loss of life and losses into the many billions of dollars.

More on the Grid: The Texas Power Crisis Didn't Have to Happen

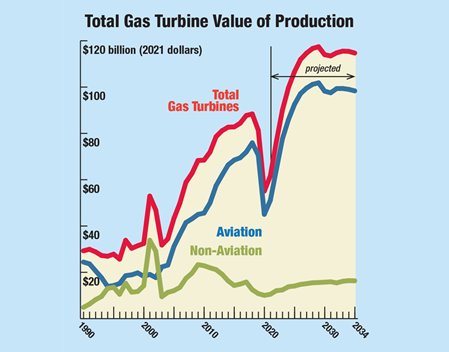

I have been surveying the gas turbine industry in this magazine each year since 1999. Over that time, the industry as a whole has seen steady growth with two large anomalies, including the plunge produced by the COVID-19 pandemic. In both the zoomed-in details and the 30,000-foot view, evidence of recovery is readily seen.

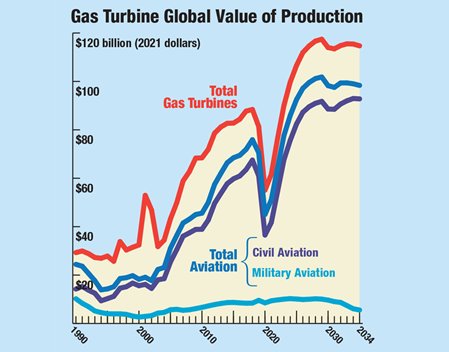

For all those years, FI has been my go-to source for data on the gas turbine worldwide market. FI reports on the total gas turbine market, dealing with both aviation (divided into commercial and military engines) and non-aviation (units for electrical power, mechanical drive, and marine systems). Using computer models and an extensive database, FI has provided the value of gas turbine manufacturing production from 1990 to 2020 and has projected values to 2034. (FI considers value of production figures to be more accurate than reported sales figures.)

As mentioned above, FI reports that the value of production for all gas turbines worldwide for 2021 was $61.6 billion, up 12 percent from a COVID induced low of $55.1 billion for 2020. As recently as 2018, the global value of production was $88.4 billion in 2021 dollars, and compared to the forecast three years ago, the accumulated lost production is $100 billion.

Virtually all of that lost value of production was in the aviation industry, which saw production valued at $51.1 billion last year, versus 2019’s forecast of $89.6 billion. FI’s value of production history over the past two decades show a steady monotonic growth for the aviation gas turbine/jet engine segment, from $18.3 billion in 2000 to $70.6 billion in 2019, then a precipitous fall to $45 billion occurred in 2020 when the COVID pandemic grounded air fleets worldwide. Recovery has now started, with FI predicting $64.4 billion for 2022, returning to pre-pandemic values in 2023. Looking into the next decade, FI sees aircraft value of production reaching $99.4 billion in 2032 as the world’s population (perhaps 9 billion by then) take to air travel.

Virtually all of that lost value of production was in the aviation industry, which saw production valued at $51.1 billion last year, versus 2019’s forecast of $89.6 billion. FI’s value of production history over the past two decades show a steady monotonic growth for the aviation gas turbine/jet engine segment, from $18.3 billion in 2000 to $70.6 billion in 2019, then a precipitous fall to $45 billion occurred in 2020 when the COVID pandemic grounded air fleets worldwide. Recovery has now started, with FI predicting $64.4 billion for 2022, returning to pre-pandemic values in 2023. Looking into the next decade, FI sees aircraft value of production reaching $99.4 billion in 2032 as the world’s population (perhaps 9 billion by then) take to air travel.

The aviation gas turbine/jet engine market has two major components. Civil aviation is the larger, at $41.7 billion in 2021, while the market for military engines, $9.5 billion in 2021, generally features more cutting-edge technology (which eventually leaks into the civil market). Currently the largest military jet engine program is Pratt & Whitney’s F135 engine, which powers all three variants of Lockheed Martin’s single-engine Lighting F-35 Joint Strike Fighter. More than 900 F135 engines, each capable of producing 40,000 pounds thrust (lbt), have been delivered. The increasing number of nations adopting the F-35—Finland and Switzerland are the most recent—means the F135 will generate aftermarket revenues for half a century. In 2011, the Pentagon designated Pratt & Whitney as the sole engine company for the F-35, so that’s a good business for the company.

Rolls-Royce won the competition to replace the engines in the Air Force’s B-52 fleet with its F130 engine.

Image: Rolls-Royce.

However, the U.S. Air Force is considering the options of either upgrading the F135 or starting an engine competition for a future replacement for the F-35s engines. General Electric Aviation, which lost a previous contest to Pratt & Whitney, is offering its XA100 adaptive cycle engine, which it is developing as part of USAF Adaptive Engine Transition Program. Given the number of airframes in the F-35 fleet, the outcome of the Air Force’s decision could reshape the fortunes of those companies.

Rolls-Royce won the competition to replace the engines in the Air Force’s B-52 fleet with its F130 engine.

Image: Rolls-Royce.

However, the U.S. Air Force is considering the options of either upgrading the F135 or starting an engine competition for a future replacement for the F-35s engines. General Electric Aviation, which lost a previous contest to Pratt & Whitney, is offering its XA100 adaptive cycle engine, which it is developing as part of USAF Adaptive Engine Transition Program. Given the number of airframes in the F-35 fleet, the outcome of the Air Force’s decision could reshape the fortunes of those companies.

Another military contract was awarded in 2021 that stands the usual military bias toward new technology on its head. Under the new $2.6 billion contract, the U.S. Air Force’s fleet of 76 Boeing B-52 Stratofortress strategic bombers will receive new engines, replacing P&W’s original TF33 engines. (As a younger engineer in the 1960s at East Hartford’s Pratt & Whitney Aircraft plant, I remember seeing the 17,000 lbt TF33 jet engines in production.) The 608 new engines, plus spares, will extend the useful life of the B-52 through the 2050s. The huge eight-engined B-52 were entered into service in 1955, so if all goes to plan, the “Big Ugly Fat Fella” will become the first 100-year-old flying jet engine powered aircraft family.

More by the Author: Bright Fortunes Await the Gas Turbine Industry

The new engine, the F130, will be produced by Rolls-Royce in Indianapolis. The 17,000-lbt turbofan engine with a 50-inch-diameter fan is the military version of its BR725 business jet engine now powering the Gulfstream 6650 and derived from the Rolls-Royce BR700 family of turbofans started by a joint venture between BMW and Rolls-Royce in 1992. In an earlier life, BMW was one of two German companies (Junkers was the other) in series production of the earliest jet engines, which means the new B-52 engines have a heritage that goes back to WWII German jet engine production.

The civil aviation market is seeing some innovative new technology nearing commercialization. In June of 2021, CFM International, the joint venture of jet engine companies GE Aviation and Safran Aircraft Engines announced its Revolutionary Innovation for Sustainable Engines (RISE) program. RISE is an open-rotor demonstration program, targeting new generation commercial jet engines for the mid-2030s.

Open-rotor engines are essentially a turbojet engine driving an exterior nacelle mounted fan (or fans), as opposed to turbofan engines where the fan is surrounded by a fan nacelle duct. The open-rotor design holds the promise of the high flight speed and performance of a turbofan, while being designed to provide the fuel economy of a slower, propeller driven turboprop engine.

Open-rotor engines are essentially a turbojet engine driving an exterior nacelle mounted fan (or fans), as opposed to turbofan engines where the fan is surrounded by a fan nacelle duct. The open-rotor design holds the promise of the high flight speed and performance of a turbofan, while being designed to provide the fuel economy of a slower, propeller driven turboprop engine.

This CFM program is a follow-on to its successful 2008 LEAP program, which has resulted in the production of 20,000-to-35,000-lbt commercial turbofan engines for single-aisle airliners.

Currently, CFM is the largest aircraft engine OEM, with over 30,000 jet engines delivered and several thousand CFM56 and LEAP engines engine deliveries per year.

The GE36 was the world’s first open-rotor aircraft engine, developed in 1984. In 2017, Safran and Avio Aero tested an open rotor as part of Europe's Clean Sky initiative. Now, CFM’s RISE program will continue to advance unducted engine design.

Image: GE Aviation.

The CFM RISE program likely will have a challenger. Pratt & Whitney, currently the largest producer of commercial aviation geared turbofan jet engines, looks to have sorted out the “new engine” problems on its 30,000 lbt PW1100G, which was first delivered in 2016. The PW1100G has achieved a competitive state of maturity and reliability and is powering more than 1,100 aircraft while delivering on its promise of a reduction of up to 20 percent in fuel consumption.

The GE36 was the world’s first open-rotor aircraft engine, developed in 1984. In 2017, Safran and Avio Aero tested an open rotor as part of Europe's Clean Sky initiative. Now, CFM’s RISE program will continue to advance unducted engine design.

Image: GE Aviation.

The CFM RISE program likely will have a challenger. Pratt & Whitney, currently the largest producer of commercial aviation geared turbofan jet engines, looks to have sorted out the “new engine” problems on its 30,000 lbt PW1100G, which was first delivered in 2016. The PW1100G has achieved a competitive state of maturity and reliability and is powering more than 1,100 aircraft while delivering on its promise of a reduction of up to 20 percent in fuel consumption.

With the current engine, featuring a 3:1 gear ratio, considered a success, Pratt plans to move on to higher thrust models, which will mean higher gear ratios. At a 4:1 ratio, for instance, the bypass ratio can be increased to 15:1. That would lead to potentially greater fuel savings, and possibly create competition for the proposed CFM RISE engines in the 2030s.

Many of these projections for civil aviation demand depend on the shape of the recovery from the pandemic and the consequences of the war in Ukraine. COVID resulted in the parking of about 14,000 jet airliners due to reduced travel demand. The engines on those planes still have service life remaining, so-called green time. Air carriers can swap green time engines into operating aircraft and thus put off new engine purchases and costly engine restorations to a later date. That could slow sales of new engines.

Meanwhile, the sanctions imposed on Russia in response to its invasion of Ukraine has left the fate of more than 500 aircraft worth more than $10 billion in limbo. Discontinuation of maintenance agreements means the engines on those planes could quickly fall into disrepair, but Russian airlines would be in no position to buy or lease replacements. The economic impact of the war is as yet uncertain, but combined with the (as of this writing) ongoing disruption from COVID, it makes for a very cloudy forecast for near-term engine sales.

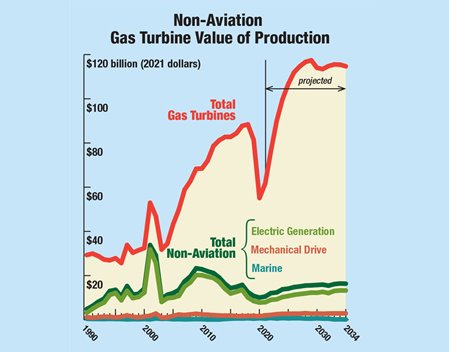

The third big market for gas turbines is electrical power generation, which had a value of production in 2021 of $8 billion. (Two other non-aviation markets are mechanical drive at $2 billion and marine turbines for propulsion and electrical power on ships, which accounted for $0.55 billion.) The electric power market saw a sharp spike in production (valued at $31.8 billion in 2021 dollars) in 2001 and a smaller but longer bump around 2010, due to energy investors overreacting to electric utility deregulation. The resulting oversupply of gas turbine electrical power plants has depressed the market in the years since.

Taking the 30,000-foot view, however, there are plenty of reasons to believe gas turbines will have a sustained and growing role in electric generation market. The most promising avenue for power-generating gas turbines is in forming part of a gas turbine combined cycle power plant (GTCC), which uses the hot exhaust from a gas turbine to make steam to drive a steam turbine.

Taking the 30,000-foot view, however, there are plenty of reasons to believe gas turbines will have a sustained and growing role in electric generation market. The most promising avenue for power-generating gas turbines is in forming part of a gas turbine combined cycle power plant (GTCC), which uses the hot exhaust from a gas turbine to make steam to drive a steam turbine.

This set-up provides by far the highest thermal efficiency yet perfected by humankind.

The authoritative 2020 Gas Turbine World Handbook list of commercially available GTCCs shows that four OEMs (GE, Siemens, Mitsubishi Hitachi, and Ansaldo) now have GTCC units with thermal efficiencies (η) between 62 percent and 64 percent in the 600-MW to 1,700-MW electrical output range. Clearly these record setting values of η are double that of power plants that existed when I was an undergraduate engineering student in the 1950s. OEMs are now aiming their GTCC development to values of η at 65 percent or higher.

The Energy Information Administration EIA data for 2020 shows that 35 percent of electricity generated in the U.S. was by natural gas combined cycle plants. Replacing coal-powered Rankine cycle power plants with gas turbine combined cycle power plants, fueled with natural gas, results in a substantial 75 percent reduction in CO₂ production per unit of electricity. The switch from coal to GTCC has resulted in a substantial reduction in CO2 emissions.

Watch the Video: When Will We See the Hydrogen Revolution?

Emissions can be reduced even further in the near future. Currently, hydrogen gas, which could be produced by electrolysis from water and surplus renewable electricity, can be combusted in GTCCs to emit only water vapor. Companies and countries are currently researching hydrogen injection into gas pipelines and networks already in use by GTCC power plants, and a number of pilot programs are in process.

It’s easy to envision a near-future power network featuring so-called green hydrogen stored in reserve that fuels a fleet of highly efficient combined-cycle gas turbines. This decoupling of the gas turbine industry from fossil fuels would ensure the industry’s continued health long into the 21st century.

In my first entry in this series of industry overviews, “The Return of Gaslight” (July 1999), I reported on the worldwide gas turbine market using Forecast International data. Adjusted into 2021 dollars, the value of production in 1998 was $30.4 billion. Twenty years later, I was able to report that the 2018 global value of production was $88.4 billion, or almost triple the initial value.

Pratt & Whitney’s PW1100G geared propulsion system has left behind its new engine problems and is delivering on its promise of quiet, efficient service.

Image: Pratt & Whitney.

That first article and most of the 23 since have been able to report a healthy industry and predictions of steady growth. Despite setbacks, those forecasts have proven largely correct. And already, the market is recovering from the calamitous impact of the global COVID-19 pandemic.

Pratt & Whitney’s PW1100G geared propulsion system has left behind its new engine problems and is delivering on its promise of quiet, efficient service.

Image: Pratt & Whitney.

That first article and most of the 23 since have been able to report a healthy industry and predictions of steady growth. Despite setbacks, those forecasts have proven largely correct. And already, the market is recovering from the calamitous impact of the global COVID-19 pandemic.

To take the very long view, I suppose one can return to the very beginning of the industrial age. In the 1791 book, The Life of Samuel Johnson, James Boswell quoted industrialist Matthew Boulton, who had partnered with James Watt to produce Watt’s innovative steam engines. “I sell here, sir, what all the world desires to have—POWER,” Boulton said. In no small measure, that desire for power and its endlessly varied applications has driven industry ever since.

The increasing need for power today is being fulfilled by gas turbines, in both flight propulsion and electrical generation. One can safely predict that the gas turbine will increase its role as a prime mover, as engineers continue to find new uses for it and improve its performance.

Lee S. Langston is professor emeritus of mechanical engineering at the University of Connecticut in Storrs and a frequent contributor to Mechanical Engineering magazine.

From the 30,000-foot perspective, the broad gas turbine industry falls into relatively few categories. The largest by far is commercial aviation, the jet engines that support the view from that altitude. Two others of smaller magnitude, military jet engines and gas turbines for electric generation, account for most of the rest of the industry.

Sometimes, however, even small markets can play an important role. Take, for example, mechanical drive gas turbines, the production of which accounted for $2 billion in 2021. That’s nothing to sneeze at, but from the perspective of the value of production for the entire gas turbine industry, which according to Forecast International (FI), a market research firm in Newtown, Conn., totaled $61.6 billion in 2021, it might be easy to overlook.

Three streams of airflow pass through and around the hot section of GE Aviation’s XA100 jet engine. The third stream (in blue) can be diverted to either add thrust or cool the engine so it can run hotter.

Image: GE Aviation

The importance of this gas turbine use was dramatically illustrated during the power crisis following the severe winter storm in Texas in February 2021. The large-scale, days-long blackout had multiple causes, but one major contributor was the failure to winterize pipeline facilities such as the compression stations. Compression station control systems malfunctioned along with other effects caused by the short-sighted economies of non-winterization, halting their function and resulting in natural gas power plants going offline for want of pipeline gas. This led to the worst energy infrastructure failure in Texas history, leading to loss of life and losses into the many billions of dollars.

More on the Grid: The Texas Power Crisis Didn't Have to Happen

I have been surveying the gas turbine industry in this magazine each year since 1999. Over that time, the industry as a whole has seen steady growth with two large anomalies, including the plunge produced by the COVID-19 pandemic. In both the zoomed-in details and the 30,000-foot view, evidence of recovery is readily seen.

Military Maneuvers

For all those years, FI has been my go-to source for data on the gas turbine worldwide market. FI reports on the total gas turbine market, dealing with both aviation (divided into commercial and military engines) and non-aviation (units for electrical power, mechanical drive, and marine systems). Using computer models and an extensive database, FI has provided the value of gas turbine manufacturing production from 1990 to 2020 and has projected values to 2034. (FI considers value of production figures to be more accurate than reported sales figures.)

As mentioned above, FI reports that the value of production for all gas turbines worldwide for 2021 was $61.6 billion, up 12 percent from a COVID induced low of $55.1 billion for 2020. As recently as 2018, the global value of production was $88.4 billion in 2021 dollars, and compared to the forecast three years ago, the accumulated lost production is $100 billion.

The aviation gas turbine/jet engine market has two major components. Civil aviation is the larger, at $41.7 billion in 2021, while the market for military engines, $9.5 billion in 2021, generally features more cutting-edge technology (which eventually leaks into the civil market). Currently the largest military jet engine program is Pratt & Whitney’s F135 engine, which powers all three variants of Lockheed Martin’s single-engine Lighting F-35 Joint Strike Fighter. More than 900 F135 engines, each capable of producing 40,000 pounds thrust (lbt), have been delivered. The increasing number of nations adopting the F-35—Finland and Switzerland are the most recent—means the F135 will generate aftermarket revenues for half a century. In 2011, the Pentagon designated Pratt & Whitney as the sole engine company for the F-35, so that’s a good business for the company.

Rolls-Royce won the competition to replace the engines in the Air Force’s B-52 fleet with its F130 engine.

Image: Rolls-Royce.

Another military contract was awarded in 2021 that stands the usual military bias toward new technology on its head. Under the new $2.6 billion contract, the U.S. Air Force’s fleet of 76 Boeing B-52 Stratofortress strategic bombers will receive new engines, replacing P&W’s original TF33 engines. (As a younger engineer in the 1960s at East Hartford’s Pratt & Whitney Aircraft plant, I remember seeing the 17,000 lbt TF33 jet engines in production.) The 608 new engines, plus spares, will extend the useful life of the B-52 through the 2050s. The huge eight-engined B-52 were entered into service in 1955, so if all goes to plan, the “Big Ugly Fat Fella” will become the first 100-year-old flying jet engine powered aircraft family.

More by the Author: Bright Fortunes Await the Gas Turbine Industry

The new engine, the F130, will be produced by Rolls-Royce in Indianapolis. The 17,000-lbt turbofan engine with a 50-inch-diameter fan is the military version of its BR725 business jet engine now powering the Gulfstream 6650 and derived from the Rolls-Royce BR700 family of turbofans started by a joint venture between BMW and Rolls-Royce in 1992. In an earlier life, BMW was one of two German companies (Junkers was the other) in series production of the earliest jet engines, which means the new B-52 engines have a heritage that goes back to WWII German jet engine production.

Innovation and Uncertainty

The civil aviation market is seeing some innovative new technology nearing commercialization. In June of 2021, CFM International, the joint venture of jet engine companies GE Aviation and Safran Aircraft Engines announced its Revolutionary Innovation for Sustainable Engines (RISE) program. RISE is an open-rotor demonstration program, targeting new generation commercial jet engines for the mid-2030s.

This CFM program is a follow-on to its successful 2008 LEAP program, which has resulted in the production of 20,000-to-35,000-lbt commercial turbofan engines for single-aisle airliners.

Currently, CFM is the largest aircraft engine OEM, with over 30,000 jet engines delivered and several thousand CFM56 and LEAP engines engine deliveries per year.

The GE36 was the world’s first open-rotor aircraft engine, developed in 1984. In 2017, Safran and Avio Aero tested an open rotor as part of Europe's Clean Sky initiative. Now, CFM’s RISE program will continue to advance unducted engine design.

Image: GE Aviation.

With the current engine, featuring a 3:1 gear ratio, considered a success, Pratt plans to move on to higher thrust models, which will mean higher gear ratios. At a 4:1 ratio, for instance, the bypass ratio can be increased to 15:1. That would lead to potentially greater fuel savings, and possibly create competition for the proposed CFM RISE engines in the 2030s.

Many of these projections for civil aviation demand depend on the shape of the recovery from the pandemic and the consequences of the war in Ukraine. COVID resulted in the parking of about 14,000 jet airliners due to reduced travel demand. The engines on those planes still have service life remaining, so-called green time. Air carriers can swap green time engines into operating aircraft and thus put off new engine purchases and costly engine restorations to a later date. That could slow sales of new engines.

Meanwhile, the sanctions imposed on Russia in response to its invasion of Ukraine has left the fate of more than 500 aircraft worth more than $10 billion in limbo. Discontinuation of maintenance agreements means the engines on those planes could quickly fall into disrepair, but Russian airlines would be in no position to buy or lease replacements. The economic impact of the war is as yet uncertain, but combined with the (as of this writing) ongoing disruption from COVID, it makes for a very cloudy forecast for near-term engine sales.

Opportunity on Land

The third big market for gas turbines is electrical power generation, which had a value of production in 2021 of $8 billion. (Two other non-aviation markets are mechanical drive at $2 billion and marine turbines for propulsion and electrical power on ships, which accounted for $0.55 billion.) The electric power market saw a sharp spike in production (valued at $31.8 billion in 2021 dollars) in 2001 and a smaller but longer bump around 2010, due to energy investors overreacting to electric utility deregulation. The resulting oversupply of gas turbine electrical power plants has depressed the market in the years since.

This set-up provides by far the highest thermal efficiency yet perfected by humankind.

The authoritative 2020 Gas Turbine World Handbook list of commercially available GTCCs shows that four OEMs (GE, Siemens, Mitsubishi Hitachi, and Ansaldo) now have GTCC units with thermal efficiencies (η) between 62 percent and 64 percent in the 600-MW to 1,700-MW electrical output range. Clearly these record setting values of η are double that of power plants that existed when I was an undergraduate engineering student in the 1950s. OEMs are now aiming their GTCC development to values of η at 65 percent or higher.

The Energy Information Administration EIA data for 2020 shows that 35 percent of electricity generated in the U.S. was by natural gas combined cycle plants. Replacing coal-powered Rankine cycle power plants with gas turbine combined cycle power plants, fueled with natural gas, results in a substantial 75 percent reduction in CO₂ production per unit of electricity. The switch from coal to GTCC has resulted in a substantial reduction in CO2 emissions.

Watch the Video: When Will We See the Hydrogen Revolution?

Emissions can be reduced even further in the near future. Currently, hydrogen gas, which could be produced by electrolysis from water and surplus renewable electricity, can be combusted in GTCCs to emit only water vapor. Companies and countries are currently researching hydrogen injection into gas pipelines and networks already in use by GTCC power plants, and a number of pilot programs are in process.

It’s easy to envision a near-future power network featuring so-called green hydrogen stored in reserve that fuels a fleet of highly efficient combined-cycle gas turbines. This decoupling of the gas turbine industry from fossil fuels would ensure the industry’s continued health long into the 21st century.

The very long view

In my first entry in this series of industry overviews, “The Return of Gaslight” (July 1999), I reported on the worldwide gas turbine market using Forecast International data. Adjusted into 2021 dollars, the value of production in 1998 was $30.4 billion. Twenty years later, I was able to report that the 2018 global value of production was $88.4 billion, or almost triple the initial value.

Pratt & Whitney’s PW1100G geared propulsion system has left behind its new engine problems and is delivering on its promise of quiet, efficient service.

Image: Pratt & Whitney.

To take the very long view, I suppose one can return to the very beginning of the industrial age. In the 1791 book, The Life of Samuel Johnson, James Boswell quoted industrialist Matthew Boulton, who had partnered with James Watt to produce Watt’s innovative steam engines. “I sell here, sir, what all the world desires to have—POWER,” Boulton said. In no small measure, that desire for power and its endlessly varied applications has driven industry ever since.

The increasing need for power today is being fulfilled by gas turbines, in both flight propulsion and electrical generation. One can safely predict that the gas turbine will increase its role as a prime mover, as engineers continue to find new uses for it and improve its performance.

Lee S. Langston is professor emeritus of mechanical engineering at the University of Connecticut in Storrs and a frequent contributor to Mechanical Engineering magazine.

The industry has hit some bumps in recent years, but the long view provides plenty of reasons for optimism.

Professor emeritus University of Connecticut Dept of Mechanical Engineering

Related Content

Jun 18, 2026

Superconductors Reimagined

Reimagined superconductors could deliver zero-resistance power under real-world conditions. The solution lies in the substrate.

May 12, 2026

The End of Brittle Solar

Flexible carbon nanotubes replace brittle ITO in perovskite solar cells, boosting durability, efficiency, and lowering costs for next generation renewables.

May 1, 2026

Quiz: Space Exploration Beyond the Moon

Artemis II has brought new excitement about the Moon, but there are plenty of missions that have gone farther.

Apr 13, 2026

The Birth of Practical Aviation

The seconds-long flight at Kitty Hawk was not the Wright brothers’ most impressive accomplishment.